Investing in the Biotech Platforms of the Future

August 18th, 2022

What are platform biotech companies, and how do their business models differ from traditional biotech companies? What are some of the critical strategic decisions in these companies’ lifecycles? What are the outcomes if things go well, or not so well? How do investors develop valuation models for platform biotech companies? We have invested in many platform biotech companies both at Gravity Fund and throughout our careers, and we’ve spent a lot of time thinking through these questions. In this deep-dive article, we take a stab at providing answers.

What are platform biotech companies?

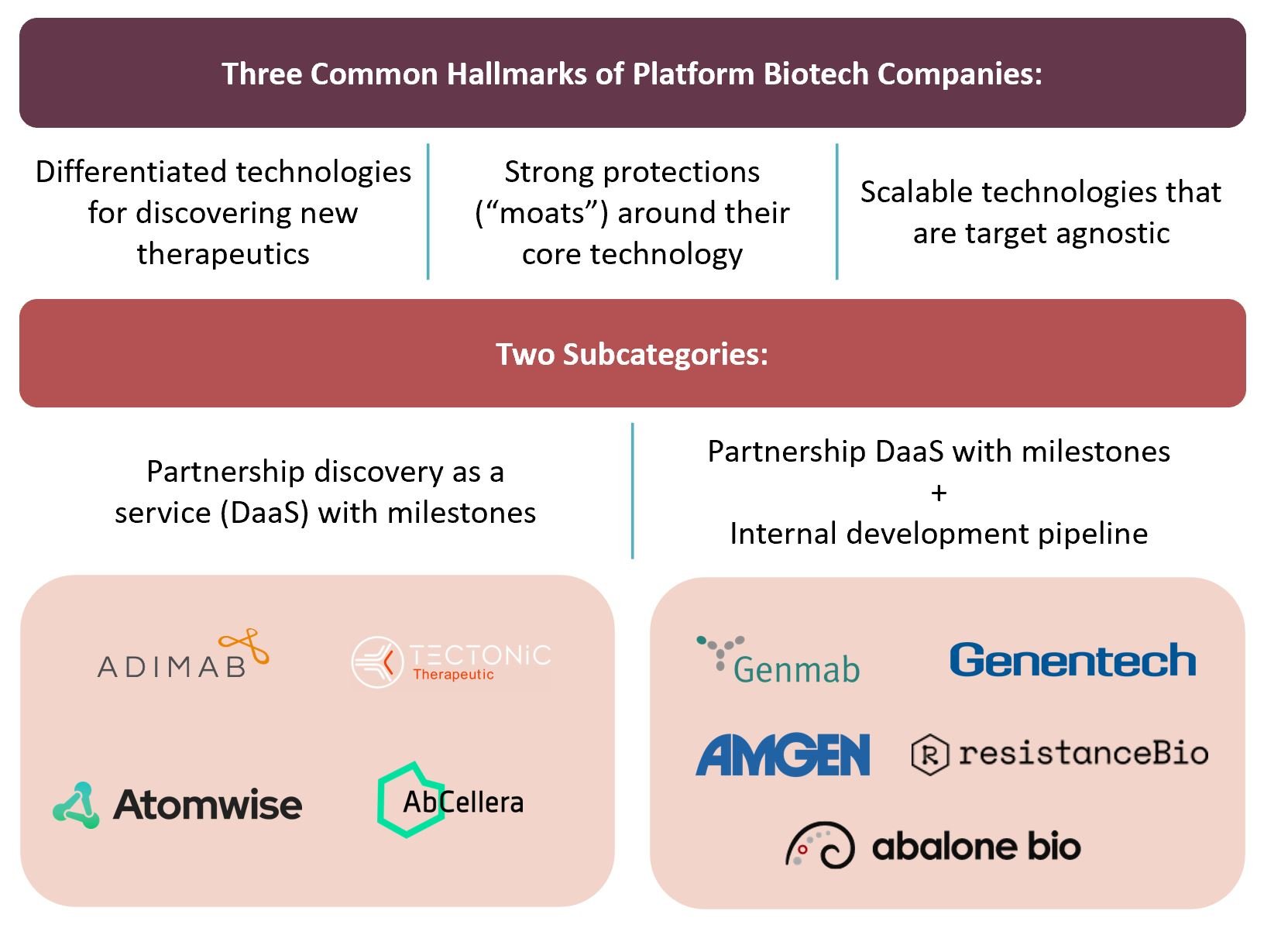

We identified three shared features and two distinct classes of platform biotech companies in the table below:

Common features:

They have differentiated technologies for discovering new therapeutics

The first part, “a differentiated technology”, is typically the necessary precursor for a platform biotech company. The technology generally expands our toolbox relative to understanding, discovering and developing new therapeutics. Oftentimes, the technology unlocks families of targets that were previously inaccessible to certain treatment modalities, or discovers new targets (or multi target approaches) to treating disease.

Side note: this analysis is centered on platform biotech companies focused on therapeutics development. Many biotech platform companies are working on adjacent sectors like synthetic biology (e.g., Ginkgo, Zymergen), services tools (e.g., Illumina, 10x genomics), and beyond. Since the business models and strategies in non-therapeutic sectors differ, each category might be worth a separate deep dive.

They have strong protections (“moats”) around their core technology

Defensible IP around the core technology is traditionally the strongest and most important moat for platform companies, but is not the only moat. Moats for platform biotech companies can be established in several other ways. For technologies that are hard to patent, such as AI algorithms for drug discovery, securing large-scale high-quality datasets is a significant moat that trains and refines the core algorithms. For therapeutic modalities in which manufacturing at scale is a major challenge, such as antibody-drugs, strategic decisions to invest in manufacturing operations and expertise can serve as an additional layer of differentiation. Oftentimes a ‘run fast’ approach to generating partnerships, while shielding core technical know-how from partners, results in a game-theory scenario which forces the hand of additional partners once a large partner becomes the first mover. In the ‘run fast’ scenario, after game-theory has run its course, embedding a platform technology into the discovery/development stacks across large pharma creates an industry wide dependency moat.

The technology is scalable and target agnostic

The true power of platform biotech companies is that they are scalable. Scalability applies to high-throughput rapid output discovery relative to a single target, as well as the platform’s ability to scale to multiple targets within a given family of targets (multiple GPCRs for example) and span multiple target families (moving from GPCRs to Ion Channels for example). A crucial component to scaling biotech platform companies that’s oftentimes underappreciated by technical founders is the ability to scale the business. Scaling the business is a function of the technology’s ability to scale, as well as organizational competencies in terms of sales, marketing, and partnership development. A high quality Chief Business Officer (CBO) is, in many cases, the most crucial hire that an early stage biotech platform company will make.

Two Subcategories

Partnership discovery as a service (DaaS) with milestones

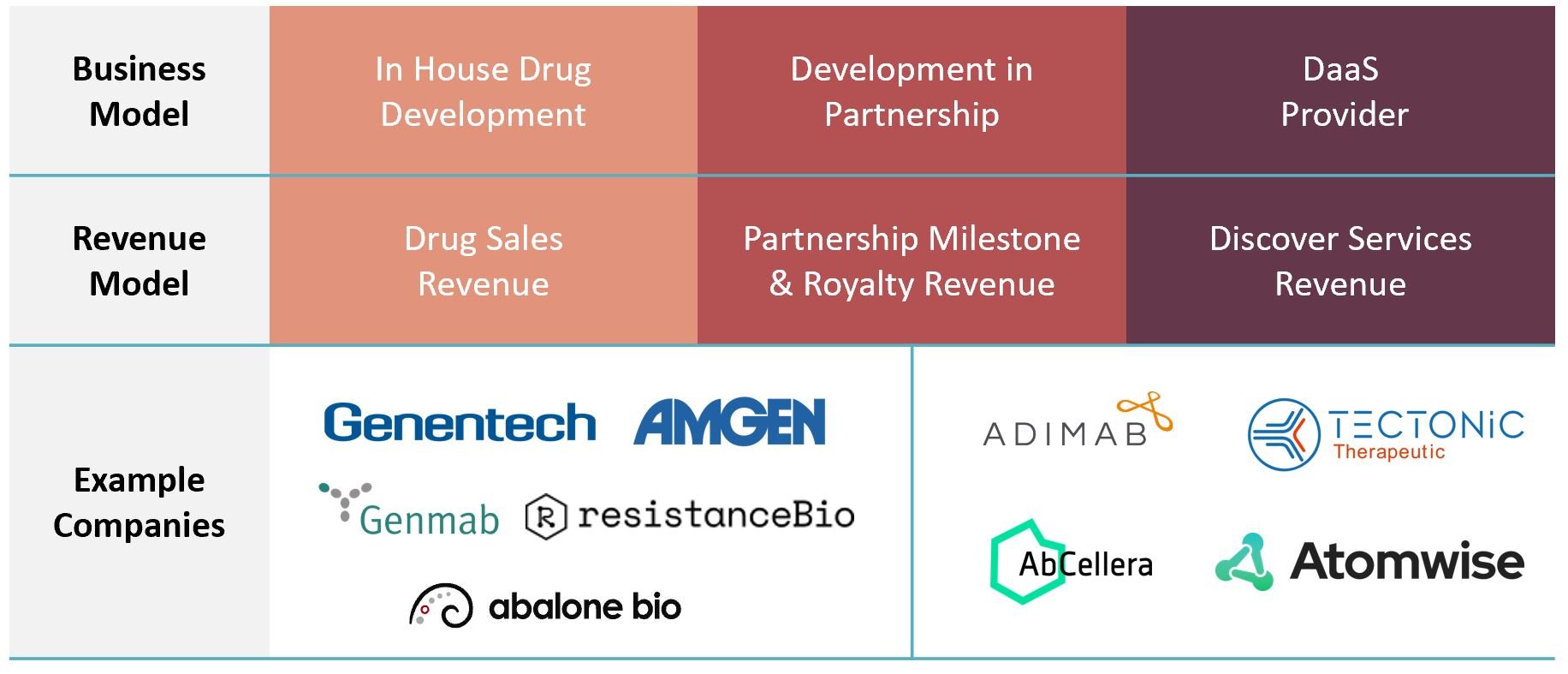

A major class of platform companies works on discovery as a service (DaaS) with pharma partners, who handle post-discovery development efforts. These platform companies expand a partner’s toolbox relative to discovering new therapeutics. In some cases, the technology unlocks families of targets that were previously inaccessible to certain treatment modalities, or discovers new targets (or multi-target approaches) to treating disease. A few examples are AbCellera (AI-powered therapeutic antibody drug discovery platform), Adimab (yeast cell-based expression platform for mAb discovery), and Atomwise (AI-powered therapeutic discovery spanning multiple treatment modalities). The revenue model for these companies includes upfront payments for services, milestones for discovery, milestones for development, and backend revenue royalties if a drug makes it to market.

Partner DaaS with milestones + internal development pipeline

These platform companies generally look very similar to the DaaS partnership category early on in their lifecycles because their outbound communication to the market is very focused upon generating DaaS partnerships with backend milestones. What differentiates this category of biotech platforms is that they have an existing or planned internal drug development pipeline which is wholly owned by the company. Oftentimes, the DaaS services offered by such companies reinforce internal development capabilities by honing discovery systems and supplementing data libraries. The classic example of this category of company is Genetech, which was a very successful DaaS partnership company in its own right, but also ran an internal development program that produced Herceptin. Herceptin was approved for HER2+ breast cancer patients in 1998 and went on to become one of the most successful drugs (therapeutically and financially) of all time. Other examples of successful companies in this category include Amgen and Genmab.

Revenue generated by biotech platforms generally falls into three buckets, (1) drug revenue income, (2) partnership income, and (3) service fee income. The following chart summarized the revenue model of each category:

How do we think about valuation difference between the subcategories of platform biotech companies?

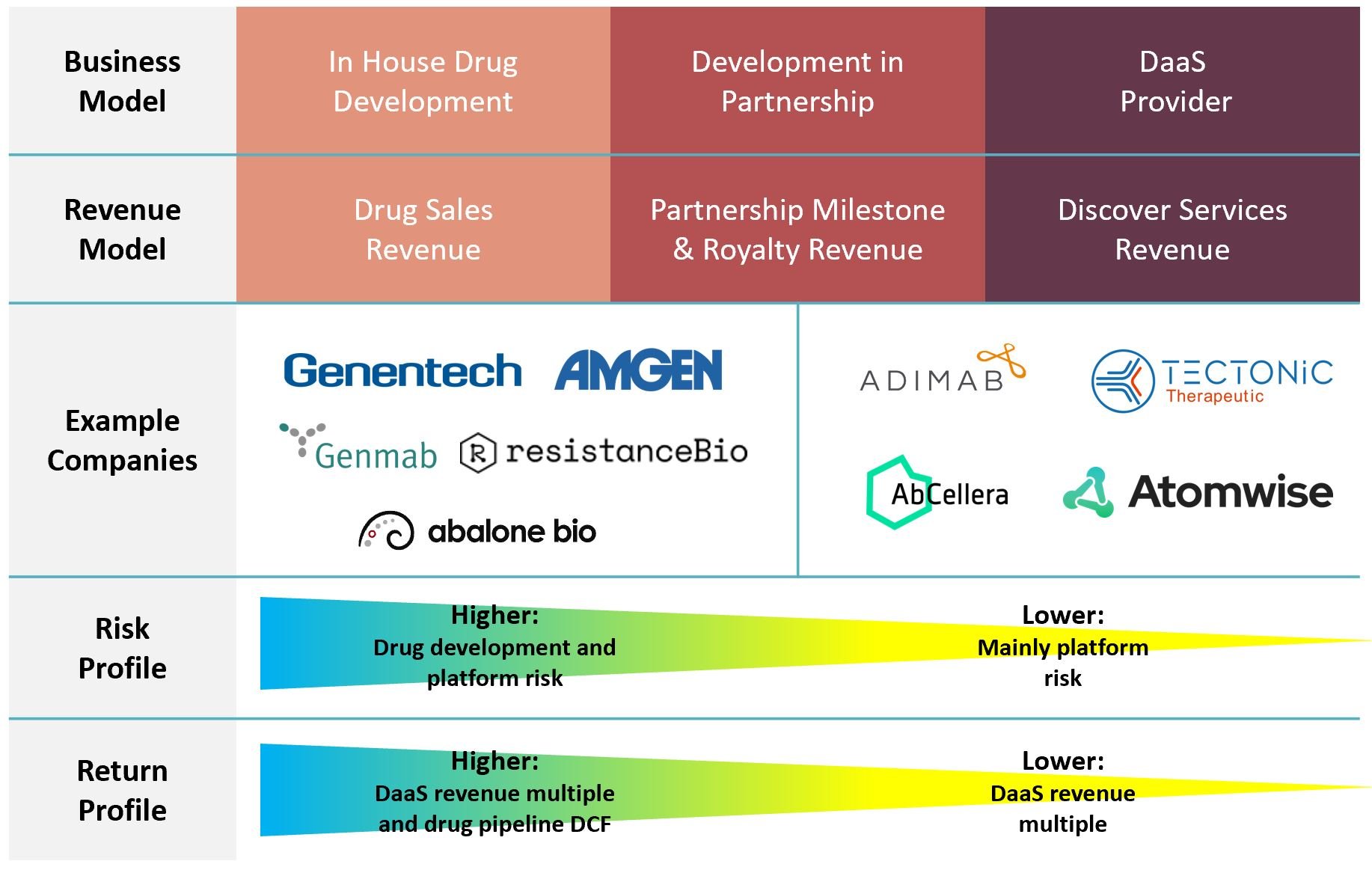

First, a comment on platform biotech (both subcategories) versus traditional biotech companies. Traditional biotech companies are asset-centric, meaning the success of the company hinges upon the clinical success of one or a handful of assets. Traditional biotech companies generally do not enter into partnerships with other pharma companies (at least not until their asset has generated significant clinical progress) and do not perform DaaS services for other pharma companies. Our thesis at Gravity Fund is that the risk adjusted return potential on traditional biotech companies simply doesn’t make sense versus the risk adjusted return potential that platform biotech opportunities present.

Why is the risk adjusted return profile more attractive for biotech platforms than traditional biotech? It’s quite simple. Traditional biotech is valued using DCF models to estimate the probability-adjusted future cash flow from lead drug candidates in the pipeline. At the earliest stages of traditional biotech companies, there’s often a small pre-clinical data set for investors to rely upon. This is very high risk, and discount rates in DCF models reflect this. As a traditional biotech company matures, it generates in-human clinical safety and efficacy data, which comes at a significant cost in terms of valuation because DCF discount rates reflect risk reduction. As the company matures and its valuation become more expensive, it also becomes more attractive to potential acquirers, and founders/investors begin contemplating an early exit. Thus, the return profile is squeezed on both ends of the spectrum, and while the risk profile has improved, the return profile has suffered.

Here are a few pairs of platform vs. traditional public companies’ market cap to illustrate the valuation premium placed on bitech platforms (numbers at Aug 16 2022 market closing):

Why is platform biotech different? The reason is primarily three-fold.

1.) Platform biotech receives DCF credit for its existing portfolio of approved drugs and development pipeline (whether via partnerships or internally), same as traditional biotech.

2.) Platform biotech pipeline potential (via partnerships or internally) is not capped in the same way traditional biotech pipelines are. The core of platform biotech is novel discovery tech, which continuously feeds pipeline development. Thus, continued pipeline expansion must be priced into valuation models, accruing pipeline value over/above the DCF value of known pipeline assets.

3.) Platform biotech discovery services alone can result in a revenue line that warrants a multi-billion dollar valuation. Value must be ascribed to that revenue line. Simultaneously, DaaS revenue provides a downside valuation marker in the event an internal pipeline doesn’t materialize, thus de-risking the opportunity.

For these reasons, at Gravity Fund, we invest in platform biotech and we don’t invest in traditional biotech. Drilling down deeper, and circling back to where we started, we invest in a subcategory of platform biotech that combines DaaS services with partnership milestones and an internal development pipeline. Segmenting platform biotech in this way allows us to further stratify our ideal biotech risk adjusted return profile.

We target early stage biotech platform companies with the potential to build out significant DaaS businesses consisting of service revenue and partnership milestone and royalty revenue, and the potential to build out compelling internal drug development programs. If the internal pipeline doesn’t develop (for reasons other than inherent problems with the DaaS tech), we generally still have the opportunity to hit our return benchmarks if the company only operates as a DaaS platform. This would typically be an exit in the $3B-$7B range, such as AbCellera or the rumored private valuations of Adimab and Atomwise. If the DaaS tech leads to a compelling internal development pipeline, the exit comps look more like Genmab ($23B), Biogen ($31B), Genentech ($47B), Gilead ($80B) or Amgen ($133B). Additionally, DaaS revenue helps fund pipeline development, minimizing investor dilution.

Platform biotech is a relatively new, open and exciting area in biotech. We’re excited to partner with early-stage entrepreneurs in this sector to help them build the next Genentech or Amgen!